Most people keep all their savings in one place. A regular savings account at whatever bank they opened when they were 18, earning somewhere around 0.40% APY, never reviewed, never moved.

That account is costing them money every month. Not dramatically. Just quietly, steadily, in a way that’s easy to ignore until you do the math.

On $10,000, the difference between a 0.40% savings account and a 4.00% high-yield account is $360 a year. On $25,000 it’s $900. The money is just sitting there. It could be doing something.

But the bigger problem isn’t rate. It’s that most people have multiple types of savings with different timelines and different rules, and they’re all in the same account. Emergency money mixed with vacation money mixed with a vague sense that there’s something in there for a down payment someday. When everything shares one account, nothing is protected.

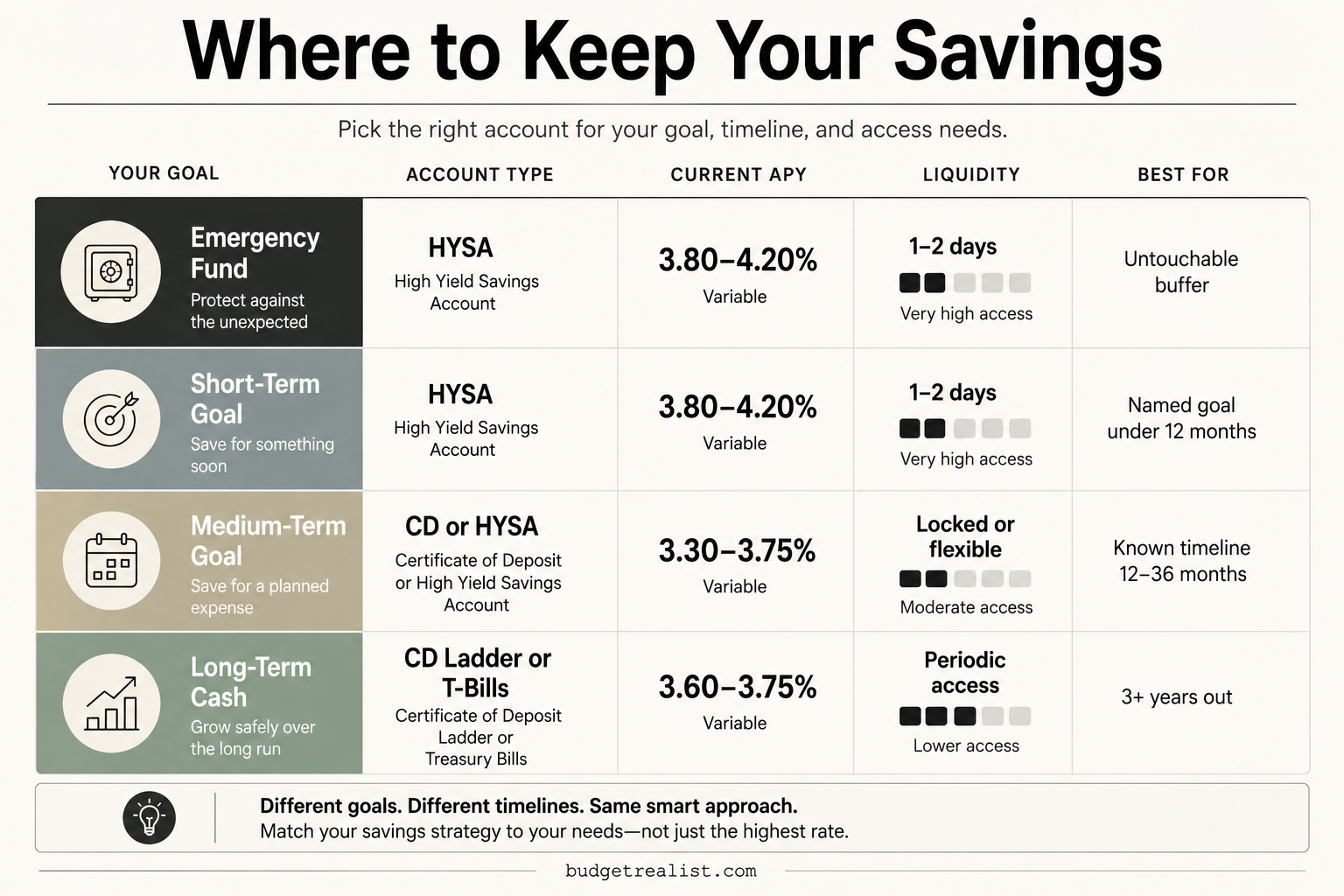

Where to keep your savings isn’t one question. It’s three, depending on when you’ll need the money.

The Right Way to Think About Where to Keep Your Savings

Every dollar you save belongs to one of three buckets. Get this wrong and the right account doesn’t matter.

Bucket 1: Emergency money. This needs to be liquid, boring, and separate from everything else. You’re not trying to grow it. You’re trying to protect it from yourself and from bad timing. Three to six months of essential expenses. Untouchable until something actually breaks.

Bucket 2: Goal money. Money you’re building toward something specific: a car, a trip, a security deposit, a down payment. It has a name and a deadline. It should earn a real return. But it needs to stay accessible because you’re going to spend it.

Bucket 3: Long-term money. Money you won’t touch for more than a year, maybe several. A house fund that’s three years out. A baby fund. A career pivot fund. Here you can trade some liquidity for a better rate.

The accounts are different for each bucket. Putting bucket 1 money in a CD because the rate is better is a mistake. Putting bucket 3 money in a checking account because it’s convenient is a more expensive one.

Match the account to the timeline. Emergency money needs liquidity above all else. Goal money needs a real return and easy access. Long-term money can lock in a rate because you know you won’t need it soon.

Where to Keep Your Savings: 4 Account Types Explained

These are the four accounts worth knowing about. One note before the breakdown: none of these are investments. You’re not trying to beat the market here. You’re trying to not lose ground to inflation while keeping your money safe and accessible.

1. High-Yield Savings Account (HYSA)

The default answer for most people in most situations. Online banks offer between 3.80% and 4.20% APY in May 2026, which is 50 to 60 times what a standard checking account pays and roughly 6 to 10 times the national savings account average of 0.61%.

HYSAs are FDIC-insured up to $250,000 per depositor. No monthly fees at the good ones. No minimums. Transfers to your linked checking account typically take one to two business days.

The slight delay is a feature for emergency funds. It kills impulse withdrawals. You can still get the money when you actually need it. You just can’t spend it because a sale ends tonight.

Best for: Emergency fund. Short-term goal savings (under 12 months). General savings buffer.

Not ideal for: Money you need same-day. Money you won’t touch for 2+ years (better options exist).

For a full breakdown of which accounts are worth opening right now, the best high-yield savings accounts in 2026 covers each one with current rates, conditions, and what to watch for in the fine print.

2. Money Market Account (MMA)

A money market account is similar to a HYSA but typically comes with check-writing privileges and a debit card. Rates in 2026 are generally in line with HYSAs, around 4.00% APY at competitive banks.

The main reason to use one over a HYSA is if you want the option to write a check or pay something directly from the account without first transferring to checking. Some people use them as a more functional emergency fund for this reason.

The downside: MMAs sometimes have higher minimum balance requirements to earn the advertised rate. Read the fine print before opening.

Best for: Emergency fund if you want debit card access. Short-term savings with occasional direct withdrawals.

Not ideal for: Long-term savings. Goal money where the debit card access creates temptation.

3. Certificate of Deposit (CD)

A CD locks your money for a fixed term in exchange for a guaranteed rate. Top short-term CDs in May 2026 are offering 3.30% to 3.75% APY on 3 to 12-month terms. Longer-term CDs offer slightly more, but the rate advantage over a HYSA has narrowed considerably since 2023 and 2024.

The defining constraint: early withdrawal penalties. Pull the money before the term ends and you give back a chunk of the interest earned. This makes CDs completely wrong for emergency funds and only appropriate for money you know you won’t need until a specific date.

The CD ladder approach solves the rigidity problem. Instead of putting $10,000 in one 12-month CD, you put $2,500 in a 3-month, $2,500 in a 6-month, $2,500 in a 9-month, and $2,500 in a 12-month. As each one matures, you have the option to spend it or roll it into a new CD. You get the rate lock without locking everything up at once.

Best for: Money you won’t need for 6 to 24 months. A down payment fund with a known timeline. Disciplined savers who benefit from the early-withdrawal deterrent.

Not ideal for: Emergency funds. Goal money with a flexible timeline. Anyone who might need to access the funds unexpectedly.

4. Treasury Bills (T-Bills)

T-bills are short-term US government debt. You buy them at a slight discount, they mature at face value, and the difference is your return. Three to six-month T-bills are currently yielding around 3.60% in May 2026.

The main advantage over a HYSA is tax treatment. T-bill interest is exempt from state and local income taxes. In a high-tax state like California or New York, that exemption can make the after-tax yield competitive with or better than a HYSA even at a nominally lower rate.

You can buy T-bills directly through TreasuryDirect or via ETFs like SGOV or BIL through any brokerage account.

Best for: High-tax state residents. Large cash reserves where the state tax exemption adds up. Savers comfortable with a brokerage account.

Not ideal for: Emergency funds. Anyone who needs same-day or next-day access. First-time savers who want simplicity.

Where to Keep Your Savings: Current Rates at a Glance

| Account Type | Current APY (May 2026) | Liquidity | Best For |

|---|---|---|---|

| Checking account | 0.07% (national avg) | Instant | Daily spending only |

| Regular savings account | 0.61% (national avg) | 1 to 2 days | Almost nothing at this rate |

| High-yield savings (HYSA) | 3.80% to 4.20% | 1 to 2 days | Emergency fund, short-term goals |

| Money market account | ~4.00% | Same day (debit card) | Emergency fund, flexible access |

| CD (3 to 12 month) | 3.30% to 3.75% | Locked (penalty to exit) | Goal money with fixed timeline |

| T-bills (3 to 6 month) | ~3.60% | Locked until maturity | High-tax states, large cash reserves |

Rates as of May 2026. Sources: FDIC for national averages, top HYSA rates from Ally, Marcus, and SoFi.

Where to Keep Your Savings Based on What You’re Saving For

Emergency fund

High-yield savings account at a different bank from your checking. Online banks like Ally, Marcus, and SoFi are the standard picks. The 1 to 2 day transfer time is intentional friction, not a drawback. It stops the fund from being raided for non-emergencies.

Do not use a CD for your emergency fund. An early withdrawal penalty on the one account you need in an actual emergency is exactly the wrong design.

Target: $1,000 to start. Three to six months of essential expenses as the final goal. Here’s how to build an emergency fund step by step.

If you’re also confused about how an emergency fund differs from a regular savings account, this breakdown of emergency fund vs savings account covers the distinction and why it matters in practice.

Short-term goal (under 12 months)

High-yield savings account. Same type of account as the emergency fund, but at a different bank and named specifically for the goal. “Vacation fund.” “Car repair buffer.” “Moving costs.” The name creates psychological separation from the emergency fund and from daily spending money.

You want this accessible because the date you’ll spend it is close and the timeline can shift.

Medium-term goal (12 to 36 months)

HYSA or CD ladder, depending on how fixed the timeline is. If you know you’re buying a car in exactly 18 months, a CD maturing around that date locks in a rate. If the timeline is fuzzy, a HYSA gives you flexibility without a significant rate penalty in the current environment.

For goals in this range, a simple split works well. Keep 50% in a HYSA for flexibility and put 50% in a 12 to 18 month CD for the rate lock. You get both.

Long-term cash reserve (3+ years)

A CD ladder or T-bills if you’re in a high-tax state. At three or more years out, you have enough visibility into the timeline to commit to fixed terms without worrying about needing the money earlier than expected.

Note: at three or more years, it’s also worth asking whether this money belongs in a cash account at all or whether it should be invested. That’s a different conversation. If the answer is definitely cash, a ladder approach gives you the best combination of yield and periodic access.

If you’re comparing specific banks for your HYSA, some have conditions buried in the fine print. SoFi’s 4.50% APY requires a qualifying direct deposit. Without it, you earn 1.00%. Always check the requirements before opening. Here’s a side-by-side comparison of Ally vs Marcus vs SoFi.

Where to Keep Your Savings: 4 Mistakes That Cost Real Money

Mistake 1: Keeping everything in a big-bank savings account

The national average savings rate is 0.61% APY. Most big banks (Chase, Wells Fargo, Bank of America) pay close to that average or less. There is no reason to keep savings there except inertia. Online banks offer the same FDIC insurance, better rates, and comparable transfer speeds. The only thing the big bank offers is a branch you probably never visit.

Mistake 2: Mixing emergency money and goal money in one account

When both live together, the emergency fund always loses. It gets spent on a flight deal or a TV sale or Christmas and then isn’t there when the furnace dies. Separate accounts with separate names solve this with no additional cost. Most banks let you open multiple savings accounts for free.

Mistake 3: Locking emergency money in a CD

Chasing an extra 0.20% in exchange for an early withdrawal penalty on the one account that needs to be available immediately is a bad trade. Emergencies don’t give you 12 months’ notice.

Mistake 4: Not knowing what rate you’re currently earning

Most people have no idea what their savings account actually pays. Log in and check. If the number has a zero before the decimal point, the account is costing you money relative to what’s available. The switch takes about ten minutes and pays for itself in days.

Will HYSA Rates Stay This High?

Probably not forever. The Fed cut rates three times in late 2025 and has held steady in 2026. The current federal funds target range is 3.50% to 3.75%. The next Fed meeting is June 17, 2026.

When the Fed cuts, HYSA rates follow within weeks. The question is how fast and by how much. Nobody can tell you with certainty, and anyone who claims they can is guessing.

What is knowable: sitting in a 0.61% savings account waiting to see what happens is costing you roughly $340 a year per $10,000 saved compared to a 4.00% HYSA. Every month you wait to move the money is money you don’t get back.

Even if rates drop to 3.00% over the next 12 months, that’s still nearly five times the national average. The case for moving your savings doesn’t depend on rates staying exactly where they are.

The Short Answer on Where to Keep Your Savings

For most people the answer is simple: a high-yield savings account at an online bank, with separate accounts for the emergency fund and each savings goal.

That one move, switching from a standard savings account to a HYSA and separating the accounts by purpose, covers 90% of what needs to happen. Everything beyond that (CDs, T-bills, laddering) is optimization for when the basics are already running.

Start there. Pick an account. Move the money. Name the buckets. The optimization can wait.

If you’re not sure which HYSA to open, this breakdown of the best high-yield savings accounts right now compares the top options with current rates and conditions. If you haven’t started your emergency fund yet, here’s how to build one from zero. And if you’re still deciding which budgeting method will free up room to save in the first place, this guide to choosing the right budgeting method will help.

")

{kind=link}