For two years I thought “high yield savings account” was a marketing trick. Like those ads that say “premium” on the packaging but it’s just regular cereal. The name sounded like something for people who had real money to invest, not for someone with $800 trying not to overdraft.

I was wrong. A high yield savings account is just a savings account that pays you more interest. That’s it. No catch, no minimum balance in most cases, no lock-in period. Just more money for doing the same thing you were already doing.

Here’s what it actually is and whether you should open one.

What Is a High Yield Savings Account

A high yield savings account (HYSA) is a savings account that pays a significantly higher interest rate than a traditional savings account. That’s the entire definition. Same FDIC insurance, same ability to withdraw your money, same basic structure. The difference is the rate.

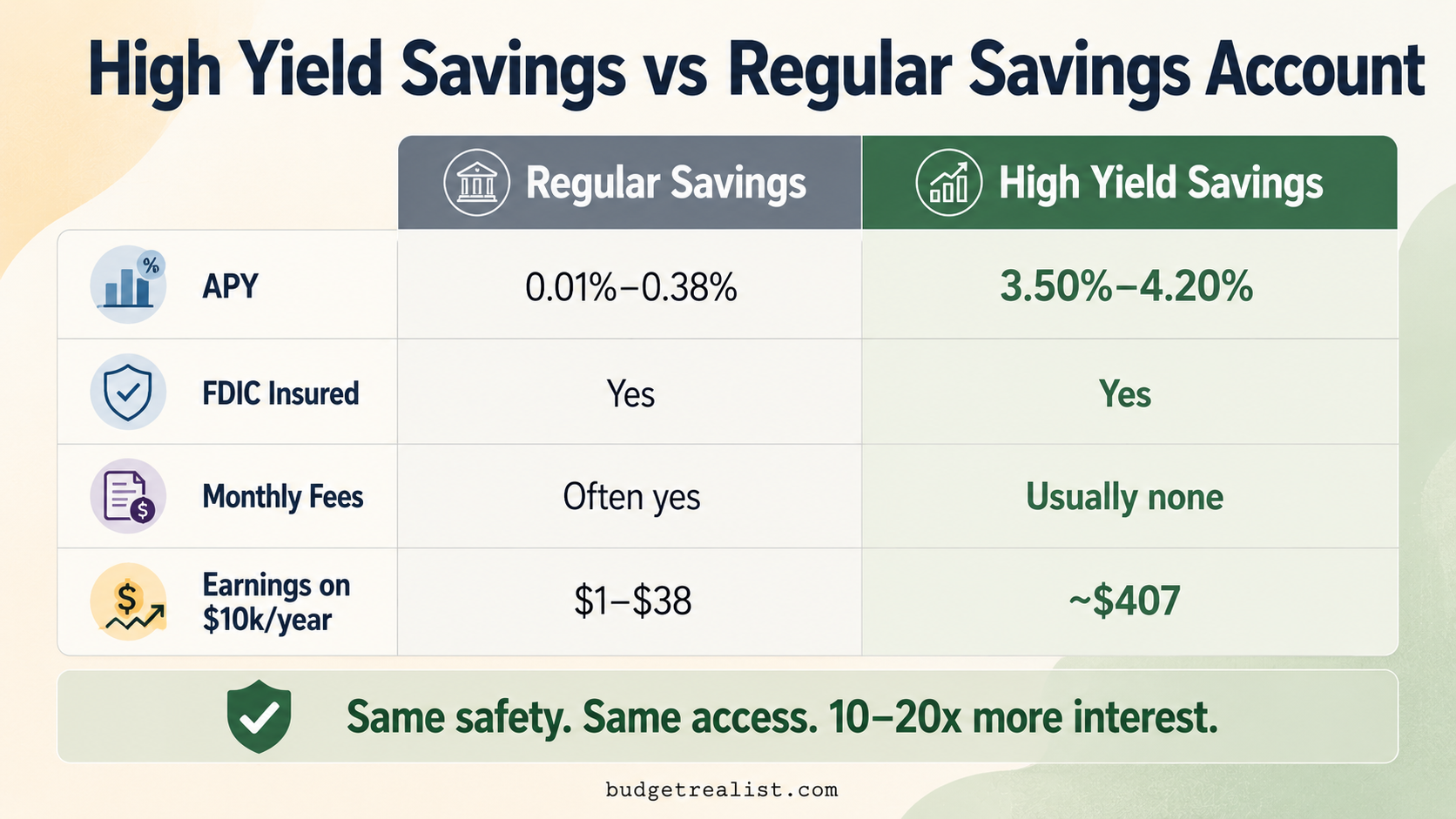

As of May 2026, the national average savings account rate is 0.38% APY according to the FDIC. The best high yield savings accounts are currently paying up to 4.20% APY. On a $5,000 balance, that’s the difference between earning $19 in a year and earning $210. Same money. Same bank account. Completely different outcome.

Most HYSAs are offered by online banks. No branches, no tellers, no ATMs to stock. Those overhead savings get passed to you as a higher interest rate. That’s why your Chase or Wells Fargo savings account pays 0.01% and an online bank pays 4%. It’s not charity. It’s a different cost structure.

A high yield savings account pays 10 to 20 times more than a standard savings account with the same safety, the same FDIC protection, and the same access to your money. The only real difference is which bank is holding it.

How Does a High Yield Savings Account Work

You open an account, deposit money, and earn interest. The mechanics are identical to any other savings account.

The interest accrues daily, meaning the bank calculates how much you’ve earned every single day based on your balance. That amount gets added to your account, usually monthly. Then the following month, you earn interest on the original deposit plus the interest that was already added. That’s compound interest, and it’s why even small balances grow meaningfully over time in a high yield account.

Here’s a concrete example. You deposit $10,000 into a HYSA earning 4% APY. You don’t touch it for a year. At the end of the year you have approximately $10,407. The same $10,000 sitting in a Chase savings account at 0.01% earns you $1. That $406 difference is real money that took you zero additional effort to earn.

The rate is variable, meaning the bank can change it. When the Federal Reserve cuts interest rates, banks typically lower their savings rates too. Rates have been declining since late 2024 as the Fed has been cutting. The best accounts are currently in the 3.50% to 4.20% range as of May 2026, down from highs of around 5% in 2023 and 2024. Still worth it by a wide margin compared to big bank rates.

High Yield Savings Account vs Regular Savings Account

| High Yield Savings | Regular Savings | |

|---|---|---|

| APY (May 2026) | 3.50% to 4.20% | 0.01% to 0.38% |

| FDIC insured | Yes ($250,000) | Yes ($250,000) |

| Minimum balance | Usually $0 | Varies |

| Monthly fees | Usually $0 | Often yes |

| Branch access | Online only (mostly) | In-person available |

| Transfer speed | 1 to 3 business days | Usually same day |

| Earnings on $10k/year | ~$407 | ~$1 to $38 |

The only real tradeoff is transfer speed. Online banks typically take one to three business days to move money to your checking account at another bank. If you’re using it as an emergency fund, pick a bank known for fast transfers. Ally, Marcus, and SoFi all have reliable transfer speeds. See how Ally, Marcus, and SoFi compare.

Is a High Yield Savings Account Safe

Yes. FDIC insured up to $250,000 per depositor per bank. The same protection that covers your checking account at Chase covers your HYSA at an online bank. If the bank fails, your money is protected.

The one thing to verify before opening any account is that the bank is actually FDIC insured. Every legitimate online bank is. You can check using the FDIC’s BankFind tool if you’re unsure. Type in the bank name and it confirms coverage instantly.

The interest rate risk is different from safety risk. Your principal is protected. The rate can go up or down. You’re not going to lose your $5,000. You might earn 3.5% instead of 4.2% if rates drop. That’s a yield change, not a safety issue.

High Yield Savings Account Pros and Cons

The pros:

You earn significantly more interest for doing nothing differently. The accounts are FDIC insured, so your money is as safe as it would be anywhere else. Most have no minimum balance and no monthly fees. Your money stays liquid, meaning you can access it without penalties whenever you need it. Setup takes 10 to 15 minutes online.

The cons:

Transfers take one to three business days to reach your checking account at another bank. If you’re using it as an emergency fund, that lag matters. Rates are variable and can drop when the Fed cuts. You’ll need to check periodically that your bank is still competitive. Some online banks have clunky apps or slow customer service. And unlike a CD, you’re not locking in today’s rate.

None of these cons outweigh the core benefit for most people. The transfer delay is manageable. The rate variability is manageable. Earning $1 a year instead of $400 is not manageable.

Some banks advertise high rates that require a minimum monthly deposit or direct deposit to qualify. Read the fine print before opening. The rate you see in the headline may not be the rate you actually earn. SoFi’s 4.00% APY, for example, requires active direct deposit. Without it, the rate drops to 1.00%.

Who Should Open a High Yield Savings Account

If you have any money sitting in a big bank savings account earning 0.01%, you should open one. Full stop. There is no scenario where earning $1 a year is better than earning $400 on the same money with the same safety.

It makes the most sense for: emergency funds, short-term savings goals (vacation, car, down payment), any money you don’t need to touch for at least a few months, and money you’re actively building up over time.

It makes less sense for: money you need to access instantly on the same day (keep that in checking), or money you’re certain you won’t need for over a year and want a locked-in rate (a CD might serve you better there). Here’s how to decide which account fits which goal.

How to Open a High Yield Savings Account

Pick a bank. Go to their website. Fill out the application. It asks for your name, address, Social Security number, and a linked bank account to fund it. The whole process takes about 15 minutes.

You’ll need to transfer money in from your existing checking account. Most banks let you do this during setup. The transfer usually takes one to two business days to clear.

Once it’s open, set up an automatic recurring transfer from your checking account on payday. Even $25 or $50 a week builds faster than you’d expect when the interest is compounding daily at 4% instead of 0.01%.

The hardest part isn’t opening the account. It’s overcoming the inertia of switching from the bank you’ve had since high school. I put it off for two years because I assumed it was complicated. It wasn’t. It was 15 minutes and a $200 opening transfer. I wish I’d done it the day I first heard about it. See our picks for the best high yield savings accounts in 2026.

A high yield savings account is a regular savings account at an online bank that pays 10 to 20 times more interest than the national average. It’s FDIC insured, has no lock-in period, and takes 15 minutes to open. If your savings are currently sitting at a big bank earning next to nothing, there is no good reason not to move them.

The money you leave at Chase earning 0.01% isn’t sitting still. It’s falling behind inflation while an online bank would have paid you 4% for holding it. That’s the cost of not knowing what a high yield savings account is. Now you know.

{kind=link}