Most people who feel like they have savings still end up in debt when something breaks. Not because they didn’t save. Because everything lived in one account with too many jobs.

The emergency fund vs savings account question sounds simple until you try to answer it with your own money. Both can live in the same type of account at the same bank. But they serve completely different jobs. When you treat them as one pile, the emergency fund always loses.

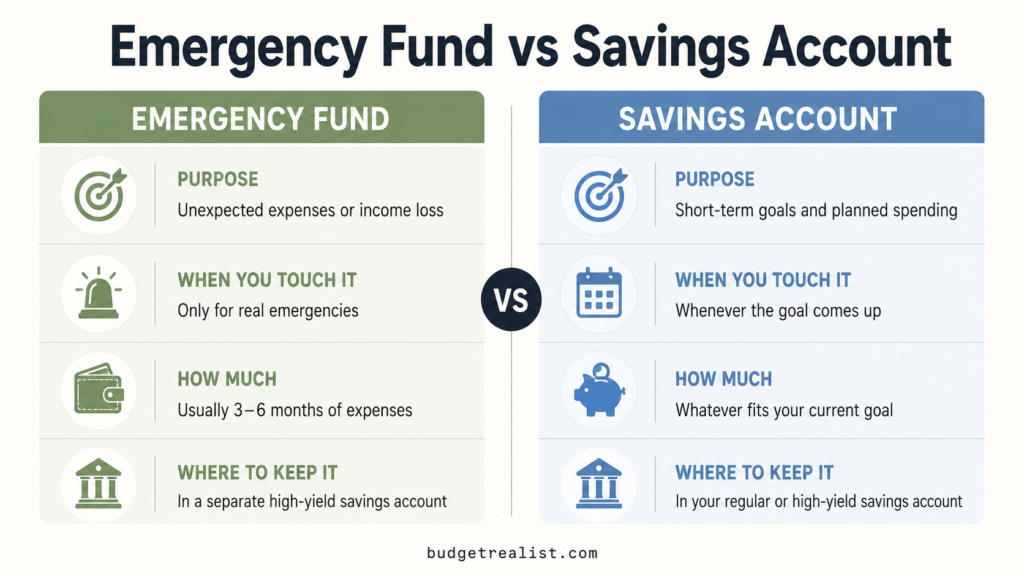

Emergency Fund vs Savings Account: The Core Difference

An emergency fund is money set aside for unexpected expenses that could otherwise break your budget. Job loss. A medical bill insurance won’t cover. A broken furnace in January. A car repair that can’t wait until payday.

The defining characteristic is that it sits idle until something forces you to use it. You’re not growing it toward anything. You’re not earmarking it for a trip or a couch or a down payment. It just sits there doing the boring but essential work of making sure one bad week doesn’t become a debt spiral.

A savings account is a vehicle, not a purpose. It’s where you park money you’re not spending right now but plan to spend eventually. A vacation in eight months. A new laptop. A security deposit. Whatever the goal is, it has a name and a timeline.

That’s the real difference in the emergency fund vs savings account debate: one is reactive, one is proactive. Emergency fund money waits for something to go wrong. Savings account money is building toward something specific.

According to a U.S. News 2026 Financial Wellness Survey of 1,216 Americans conducted in January 2026, 43% of Americans couldn’t pay for a $1,000 emergency expense with their savings. A separate June 2025 Empower study found 1 in 3 Americans have zero emergency savings. And Bankrate’s Emergency Savings Report, based on December 2025 polling, found 29% of Americans carry more credit card debt than emergency savings.

That last number is worth sitting with. Nearly a third of Americans are one car repair away from putting it on a card at 22% interest.

Why the Emergency Fund vs Savings Account Confusion Happens

Both can sit in the exact same type of account at the same bank. A high-yield savings account works for both. The separation is in how you label the money and, more importantly, what rules you apply to each pile.

The U.S. News 2026 survey found that 44% of Americans don’t consider their emergency fund and savings account to be separate. That’s nearly half the country treating them as one pile. It explains a lot about why so many people feel like they have savings and still end up in debt when something breaks.

Here’s what happens in practice. You have $2,400 in one account. You think of it as an emergency fund. You also think of it as vacation money.

In September, flights are on sale. You book. Spend $600. In November, the tires. Another $500. In March, the water heater dies. Replacement is $1,100. You’re now at $200, stressed, and probably putting the remaining $900 on a credit card.

Nothing about that is unusual. It’s what happens when one account serves too many masters.

The emergency fund vs savings account difference is about purpose and rules, not account type. Both can be high-yield savings accounts. But one has strict withdrawal rules. The other is there to be spent on your goals.

Should Your Emergency Fund Be Separate From Your Savings Account?

Yes. Keep them in separate accounts, ideally at a different bank from your checking account.

This isn’t just an organizational preference. It’s a behavioral guardrail. When your emergency fund and savings account are one account, the emergency fund label is the only thing protecting that money from non-emergency spending. That’s not enough protection. Labels are easy to ignore when a flight deal expires in six hours.

Moving the emergency fund to a different bank adds two business days to any transfer. That friction kills impulse withdrawals. Not because you can’t access the money, but because the delay forces you to actually decide whether something is a real emergency. Most things that feel urgent at 11pm don’t pass that two-day test.

Don’t lock your emergency fund in a CD chasing a slightly better rate. CDs charge early withdrawal penalties, which means your “emergency” money isn’t actually available in an emergency. Liquid always beats yield for this specific account.

Where to Keep Each: Emergency Fund vs Savings Account Options

Both accounts should earn interest. Letting money sit in a standard checking account or a low-yield savings account at a big bank is leaving real money on the table. The national savings average is 0.61% APY. Top high-yield savings accounts are paying over 4%.

For the emergency fund, a high-yield savings account at an online bank is the right move. Ally, Marcus by Goldman Sachs, and SoFi all offer competitive rates with fast transfer speeds. The key requirement is liquidity: you need to be able to access the money within one to two business days without penalties. See the best high-yield savings accounts right now.

For the savings account, the same type of account works, but you have more flexibility. If your goal is more than 12 months away, a CD ladder can make sense. If it’s shorter, a high-yield savings account keeps it accessible.

One thing that applies to both: FDIC insurance. The Federal Deposit Insurance Corporation insures deposits up to $250,000 per depositor, per bank. If you split your emergency fund and savings across two different banks, each account is separately insured up to that limit.

How Much Goes in Each Account

These two don’t compete. You build them in order, then run them at the same time.

Before anything else. Before the vacation savings, before extra debt payments. This is the fire extinguisher. It doesn’t need to be big yet. It just needs to exist and be untouchable.

Once the $1,000 is locked away, open a second account for actual goals. Name it something specific: “Vacation 2027,” “Car fund,” “Moving costs.” Give it a target number and a deadline.

The $1,000 is a floor, not the goal. Build toward three months of essential expenses, then six. Most people split their monthly savings contribution: part goes to the emergency fund until it’s fully funded, the rest goes to the savings goal account. Here’s the full guide to building your emergency fund step by step.

3 Mistakes People Make With the Emergency Fund vs Savings Account Setup

Mistake 1: Treating the emergency fund as a savings account with stricter rules. You can’t willpower your way out of mixing them. The accounts need to be physically separate. Intention alone doesn’t work when you can see the balance.

Mistake 2: Not starting the savings account until the emergency fund is fully funded. It takes most people one to three years to build a full emergency fund. Waiting that long to start working toward any goal makes the whole process feel punishing. Run both at once with a split contribution.

Mistake 3: Keeping the emergency fund somewhere inconvenient. If it’s too hard to access, you won’t fund it consistently. If it’s too easy, you’ll spend it on non-emergencies. The sweet spot is a different bank from your checking, with same-day or next-day transfer capability.

The Emergency Fund vs Savings Account Difference Comes Down to Purpose

The emergency fund sits there waiting for something to go wrong. The savings account is building toward something you want. Both matter. Both should be earning interest. Neither should be in the same account.

Separate them. Name them. Put them at different banks if you need the friction to keep yourself honest. Once both are running, the stress of unexpected expenses drops considerably. Not because emergencies stop happening, but because you stop putting them on a card.

If you haven’t started building your emergency fund yet, this step-by-step guide to building an emergency fund walks through exactly how to get to $1,000 and beyond. And if you’re deciding where to park the money once it’s set aside, the best high-yield savings accounts right now are paying over 4% APY.

")

{kind=link}