Most comparison articles on ally vs marcus vs sofi say the same thing in different fonts. Rate table at the top, vague pros and cons, affiliate links at the bottom. No clear answer on which one to actually pick.

The reason the decision feels hard is that all three are genuinely good accounts. None of them are traps. The differences that matter are specific to your situation, and once you know which situation you’re in, the answer is usually obvious.

Here’s the ally vs marcus vs sofi comparison broken down by what actually differs, not by what sounds impressive in a bullet point.

[ADD HERO IMAGE HERE — Alt: person comparing ally vs marcus vs sofi savings account rates on laptop]

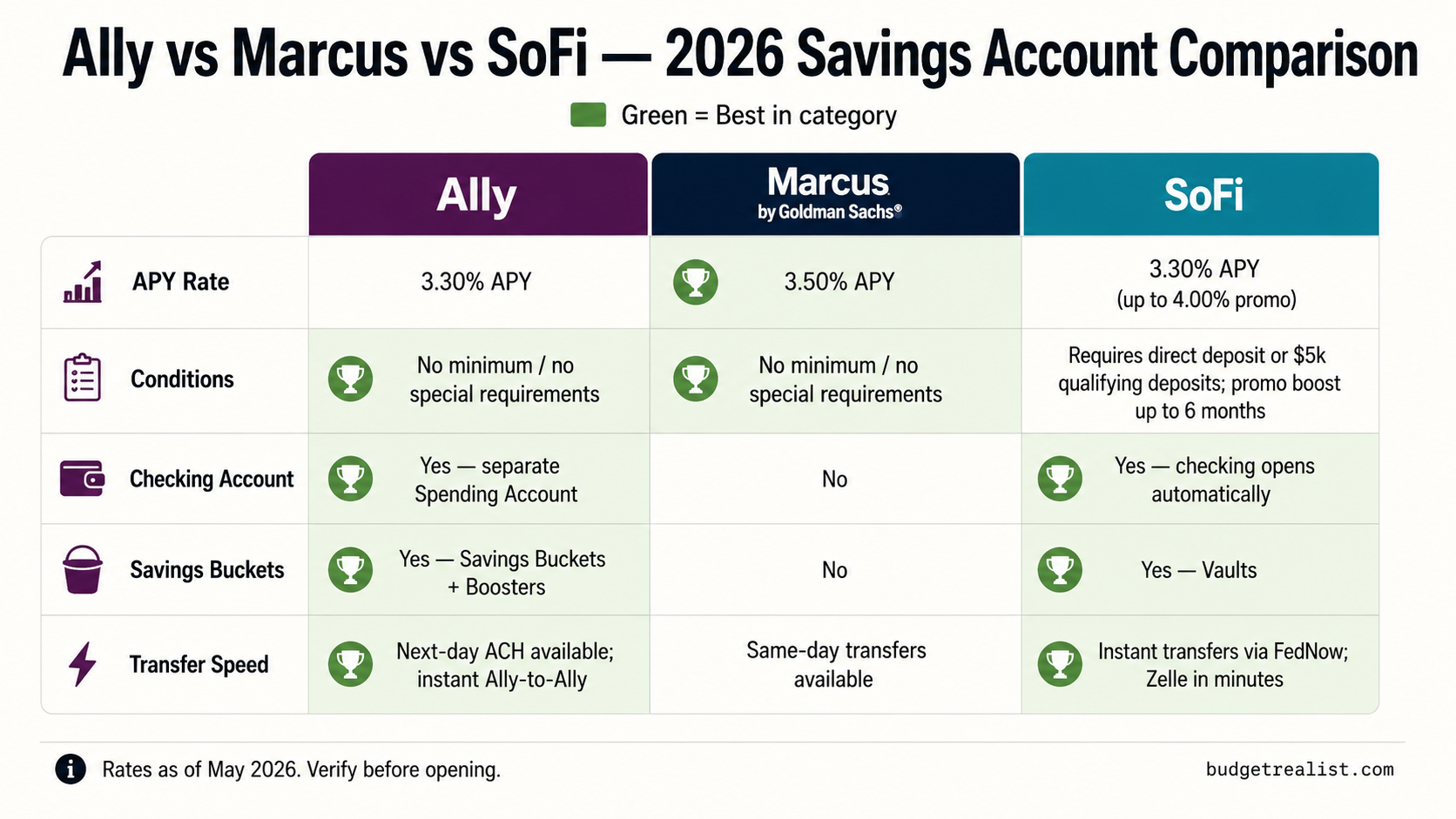

Ally vs Marcus vs SoFi: Current Rates (May 2026)

| Bank | APY | Condition | Minimum |

|---|---|---|---|

| SoFi | 4.00% | Requires direct deposit | $0 |

| Marcus | 3.50% to 4.10% | None | $0 |

| Ally | 3.30% | None | $0 |

| Rates as of May 2026. APYs change frequently. Verify on each bank’s site before opening. | |||

SoFi has the highest rate. But that 4.00% requires an active direct deposit, meaning your paycheck or government benefits routed directly to SoFi. Without it, the rate drops to 1.00%. That’s a 75% rate cut for not switching your payroll.

Marcus and Ally pay their rates to everyone, unconditionally, on day one. That distinction is the most important thing to understand in the ally vs marcus vs sofi comparison before anything else.

Ally vs Marcus vs SoFi: SoFi Breakdown

SoFi is not a standalone savings account. It’s a checking and savings combo that you can’t separate. When you open a SoFi account, you get both. The savings portion earns 4.00% APY with direct deposit. The checking earns 0.50% APY.

That bundling is either a feature or a problem depending on the situation.

For someone willing to make SoFi their primary bank and route their paycheck there, the package is genuinely strong: highest rate on this list, a checking account, 55,000+ Allpoint ATMs, and a $50 to $400 welcome bonus through December 2026 depending on direct deposit amount.

For someone who wants a standalone savings account to park money separately from day-to-day spending, SoFi is the wrong tool. Without direct deposit the rate is 1.00%, which is worse than both Marcus and Ally with no conditions attached.

You’re willing to make it your primary bank. Your paycheck goes in via direct deposit. You want one app that handles checking, savings, and the option to invest later. You want the welcome bonus. If that’s not you, keep reading.

Ally vs Marcus vs SoFi: Marcus Breakdown

Marcus is what it says it is. A high-yield savings account backed by Goldman Sachs. No checking. No debit card. No ATM access. No gimmicks.

The rate is currently 3.50% to 4.10% APY with no minimum balance and no fees. You link it to your existing checking account at another bank and move money back and forth via ACH transfer. Marcus processes same-day transfers up to $100,000 if submitted before noon ET, which is faster than both Ally and SoFi.

The Goldman Sachs backing matters more to some people than others. For larger balances, $20,000 or $30,000 and above, the institutional credibility carries weight that Ally and SoFi don’t have in the same way.

The downside is exactly what it looks like: no ecosystem. No checking account. No buckets or sub-accounts. No investing integration. Marcus does one thing well and nothing else.

You already have a checking account you like and want somewhere better to park savings. You want a no-conditions rate. You have a larger balance and want Goldman Sachs behind it. You don’t need sub-accounts or budgeting features.

Ally vs Marcus vs SoFi: Ally Breakdown

Ally has the lowest rate of the three at 3.30% APY, unconditional. But Ally has built more savings infrastructure than any other online bank in this category since 2009.

The feature that separates Ally in the ally vs marcus vs sofi comparison is Savings Buckets. One account, up to 30 labeled sub-accounts. Emergency fund in one bucket. Vacation in another. New car in another. Each has its own balance and progress bar, all earning the same 3.30% APY, all under one login.

The behavioral impact of this is real. When savings is one undivided balance, the emergency fund gets raided for non-emergencies because the separation doesn’t feel real. With labeled buckets, the visual separation creates a psychological barrier that makes goal money feel off-limits. It’s a small design choice that changes how people actually behave with their money.

Ally also offers Surprise Savings, which analyzes a linked checking account and automatically moves small amounts to savings when the balance can absorb it. A full checking account option. And $10 per month in out-of-network ATM reimbursements.

The 0.70% rate gap between Ally and SoFi with direct deposit is real. On $10,000 that’s $70 per year. On $30,000 it’s $210. Whether that gap justifies switching an entire banking relationship to SoFi is a personal call.

You want to organize multiple savings goals in one place. You want a bank with a long track record and full checking integration. You tend to raid savings for non-emergencies and need the visual separation that buckets provide. The highest rate is not your only priority.

Ally vs Marcus vs SoFi: Full Feature Comparison

| Feature | Ally | Marcus | SoFi |

|---|---|---|---|

| APY (unconditional) | 3.30% | 3.50%+ | 1.00% |

| APY (with conditions) | N/A | N/A | 4.00% (direct deposit) |

| Checking account | Yes | No | Yes (bundled) |

| Savings buckets | Yes (up to 30) | No | Yes (Vaults) |

| ATM access | 43,000+ Allpoint | None | 55,000+ Allpoint |

| Welcome bonus | None | None | $50 to $400 |

| Transfer speed | 1 to 3 days | Same-day (under $100k) | 1 to 3 days |

| FDIC insured | Yes ($250k) | Yes ($250k) | Yes (up to $2M via sweep) |

| Best for | Goal organization | Pure savings, larger balances | Primary bank switchers |

Ally vs Marcus vs SoFi: Which One to Actually Pick

Pick SoFi if you’re ready to make it your primary bank and move your direct deposit. The 4.00% APY plus the welcome bonus makes the switch worth it on paper. Just understand you’re signing up for a full banking relationship, not a side savings account.

Pick Marcus if you already have a checking account you’re happy with and want the best unconditional rate on a pure savings account. No ecosystem, no features, just a competitive rate and Goldman Sachs behind it. Marcus also wins on transfer speed in the ally vs marcus vs sofi comparison, which matters if quick access is a priority.

Pick Ally if organization is the problem. If savings gets raided for things that aren’t actually emergencies, Savings Buckets is the fix. The rate is slightly lower but the behavioral infrastructure is the best of the three. Ally also works well as a full checking replacement.

Running two of them is also a legitimate strategy. Marcus for the emergency fund because of same-day transfer speed and the unconditional rate. Ally for everything else because the buckets keep goals visually separated. Neither account has fees, so there’s no cost to running both. More on how to decide what goes where.

All three rates are variable. The Fed has held steady in 2026 but analysts expect more cuts. The rates you open with today are not guaranteed to stay there. Check your rate every few months and compare. A bank that was competitive in January might not be in July.

The Ally vs Marcus vs SoFi Decision Is Simpler Than It Looks

The ally vs marcus vs sofi comparison comes down to one question: do you want the highest rate or the most useful features?

SoFi wins on rate if you switch your direct deposit. Marcus wins on rate if you don’t want any conditions. Ally wins on features if you need buckets and a full banking ecosystem.

None of them are a bad choice. Any of them beats leaving money at a big bank earning 0.01%. Pick one, open it today, and move your savings. The difference between choosing perfectly and choosing well is much smaller than the difference between choosing well and doing nothing.

If you’re still building your emergency fund, here’s how to get to $1,000 and beyond. And if you want to understand what a high-yield savings account actually is before opening one, this guide to what is a high yield savings account covers the basics clearly.

")

{kind=link}