For three years, I had $4,000 sitting in a Chase savings account. It earned $1.20 in interest one year. One dollar and twenty cents. I bought a coffee with that, felt mildly guilty, and moved on.

The thing is, I knew high-yield savings accounts existed. I’d seen the ads. I just assumed there was a catch somewhere. Nobody hands you 4% for nothing, right?

There was no catch. I was just leaving money on the table because I didn’t understand the options. So here’s the breakdown I wish someone had given me.

Where to Put Savings for Best Return: Start With This Question

Before comparing rates, you need to answer one question: when do you need this money?

Your time horizon determines everything. Money you might need next month belongs somewhere different than money you’re parking for two years. Get this wrong and you’ll either lock up cash you need or leave it somewhere so liquid it earns almost nothing.

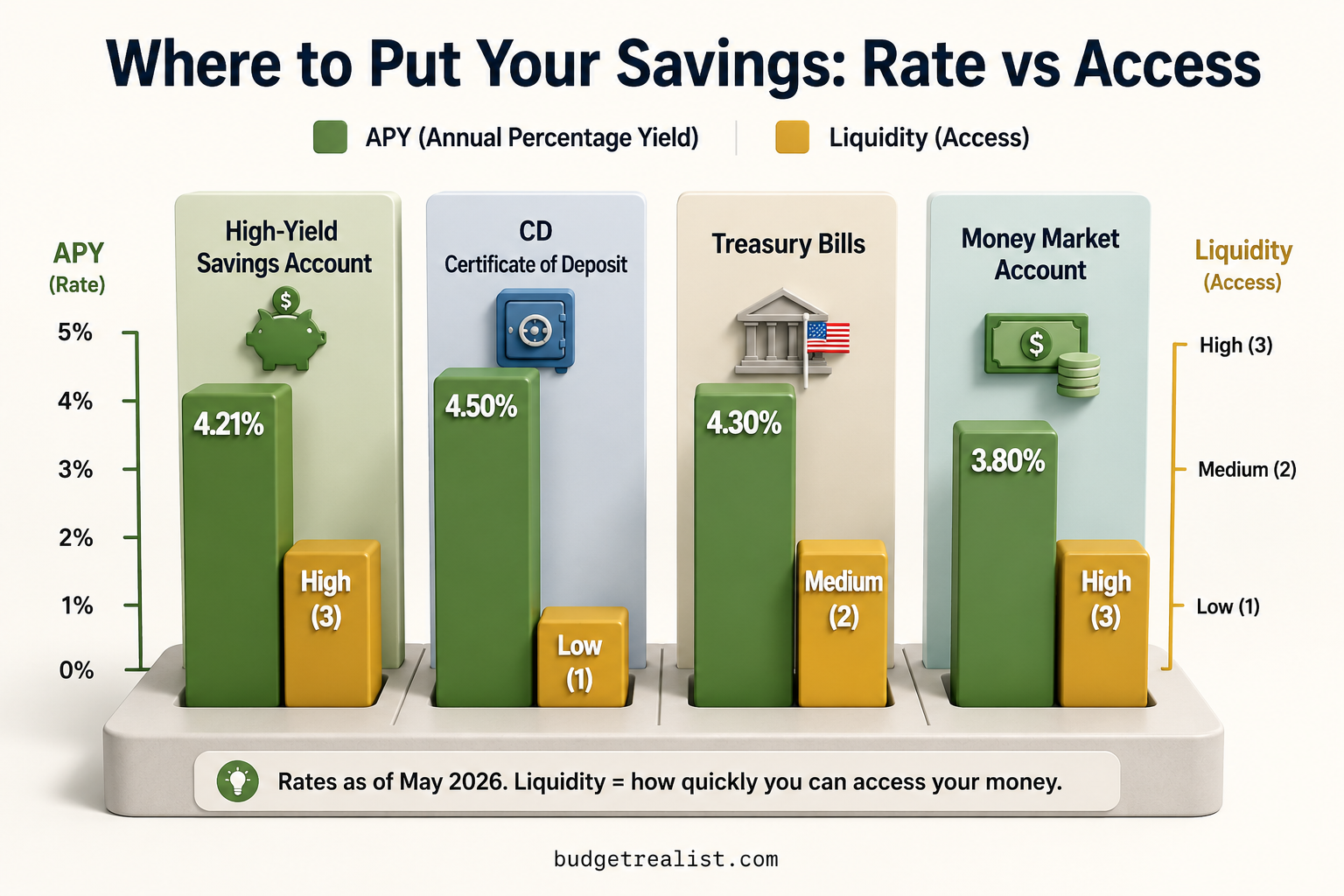

According to the FDIC, the national average savings account rate was 0.38% APY as of December 2025. Meanwhile, the best high-yield savings accounts are currently paying up to 4.21% APY. On a $10,000 balance, that’s the difference between earning $38 in a year and earning $421. Same money, same risk, wildly different outcome.

A Santander survey found that 70% of Americans aren’t yet using higher-yield accounts. Which means most people reading this are in the same boat I was: money parked somewhere comfortable, slowly losing ground to inflation.

The best place to put savings for the best return is the one that matches your timeline. For most people with everyday savings goals, a high-yield savings account wins on every dimension: rate, safety, and access. The other options are better in specific situations.

Option 1: High-Yield Savings Account (HYSA)

Best for: Emergency funds, short-term goals, money you might need within 12 months.

A high-yield savings account works exactly like a regular savings account, except the rate is dramatically better. Online banks can offer higher rates because they don’t have branches to maintain. No ATMs to stock. No tellers. Those overhead savings go directly into your APY.

Current top rates are running around 4% to 4.21% APY as of May 2026. That’s roughly 10 times the national average. The money stays FDIC-insured up to $250,000, there’s no lock-in period, and you can withdraw whenever you need to.

The one thing to check before opening: transfer speed. Some online banks take two to three business days to move money to your checking account. That’s fine for planned spending. For emergencies, you want same-day or next-day transfers. Ally, Marcus by Goldman Sachs, and SoFi all have fast transfer options. See our full picks for the best high-yield savings accounts in 2026.

The downside: Rates are variable. If the Federal Reserve cuts rates, your APY drops. You’re not locking in today’s rate forever. In 2026, some analysts expect rates to ease toward 3% to 3.5% as the Fed continues adjusting policy. Still beats 0.38% at your big bank, but worth knowing.

Option 2: Certificates of Deposit (CDs)

Best for: Money you won’t need for a set period and want a guaranteed rate on.

A CD is a deal you make with a bank: you agree to leave your money for a fixed term (three months, one year, five years), and they agree to pay you a fixed rate the whole time. No surprises. No rate drops if the Fed moves.

Current CD rates are competitive with HYSAs, and in some cases slightly higher, especially on longer terms. The tradeoff is inflexibility. Pull money out early and you’ll pay an early withdrawal penalty, often equal to several months of interest.

The sweet spot for most people is a CD ladder: instead of putting everything into one long-term CD, you split it across multiple CDs with staggered maturity dates. Some matures in three months, some in six, some in a year. You get predictable access to portions of your money at regular intervals without sacrificing the higher rate entirely.

Never put your emergency fund in a CD. The whole point of an emergency fund is that you can access it immediately. Early withdrawal penalties will eat into the interest you earned, which defeats the purpose. CDs are for savings goals with a known, fixed timeline.

Option 3: Treasury Bills (T-Bills)

Best for: People in high-tax states who want a safe, predictable return and can leave money parked for 4 to 52 weeks.

Treasury bills are short-term US government debt. You buy them at a discount, they mature at face value, and the difference is your return. They’re backed by the federal government, which makes them about as safe as it gets.

Current T-bill yields are broadly comparable to top HYSA rates. But here’s the part most people miss: T-bill interest is exempt from state and local taxes. If you live in California, New York, or another high-tax state, that tax exemption can make T-bills more attractive than a HYSA with a similar headline rate, because your after-tax return is higher.

The catch: T-bills are less liquid than a HYSA. You buy them with a fixed term, and while you can sell them before maturity on the secondary market, it adds friction. They’re not the right choice if you might need the money suddenly.

You can buy T-bills directly through TreasuryDirect.gov with no fees or through a brokerage account.

Option 4: Money Market Accounts

Best for: People who want HYSA-level rates but also want check-writing or debit card access.

A money market account is essentially a hybrid between a savings account and a checking account. It typically offers higher rates than a traditional savings account, sometimes comparable to HYSAs, while also giving you the ability to write checks or use a debit card directly from the account.

The downside is that the top rates are usually not quite as high as the best HYSAs. You’re paying for the added convenience with a slightly lower yield. They’re also sometimes FDIC-insured (bank money market accounts) but not always. Money market funds at brokerages are covered by SIPC instead, which is a different protection structure.

Don’t confuse a money market account with a money market fund. The account is a bank product. The fund is an investment product. Similar name, different structure, different risk profile.

The Decision Framework: Which Option Is Right for You

| If you need the money… | Best option |

|---|---|

| Within 1 to 3 months | HYSA or money market account |

| In 6 to 12 months, exact date known | Short-term CD or T-bill |

| In 1 to 3 years, flexible date | CD ladder or HYSA |

| Emergency fund (no set date) | HYSA at a separate bank |

| Not sure yet | HYSA until you decide |

The “not sure yet” row is more common than people admit. If you don’t have a clear timeline, a HYSA is the right default. It earns a competitive rate, it’s liquid, and you can move the money the moment you know where it belongs.

What I Did Wrong (And What I Do Now)

After three years of watching Chase pay me essentially nothing, I finally moved my savings to an online bank. Setup took about 15 minutes. I linked it to my checking account and set up a weekly auto-transfer.

The first year I earned just over $200 in interest on a balance that averaged around $5,000. That’s not life-changing money. But it covered two months of groceries, which is more than nothing, and considerably more than the $1.20 I was earning before.

I now run three accounts: one HYSA for my emergency fund at a bank that transfers fast, one HYSA for shorter savings goals, and I’ve started experimenting with T-bills for a larger chunk I know I won’t need for six months. The tax exemption actually matters at my income level and state.

None of this required a financial advisor. It required understanding that “savings account” is not one thing. It’s a category, and within that category, some options pay you 10 times more than others for the exact same level of risk.

The best place to put savings for the best return is the one that fits your actual timeline. For most people, that’s a high-yield savings account: safe, liquid, and paying rates that are genuinely competitive right now. If you have money you know you won’t touch for six months or more, a CD or T-bill can get you a fixed rate that won’t move when the Fed does.

The worst option is doing nothing. Leaving money at a big bank earning 0.01% while online banks pay 4% is the most expensive kind of inertia. Your money should be working harder than that. Not sure which account is for what? Start here.

")

")

{kind=link}