The extreme frugal living content you find online falls into two categories. The first is the $200k salary person who saved 85% of their income and wants credit for it. The second is a listicle of 47 tips that treats making your own dish soap as equivalent in importance to restructuring your housing costs.

Neither is useful for someone on a normal income trying to figure out how aggressively they can actually cut without their life becoming a punishment.

Here is the honest version. What extreme frugal living looks like at realistic income levels, which aggressive cuts are worth making, which ones have hidden costs that make them not worth it, and where the line is between disciplined and counterproductive.

What Extreme Frugal Living Actually Means on a Normal Income

The viral extreme frugal living stories almost always involve high incomes. Bradley on a Budget earned $234,479 in 2025 and spent $33,100, saving 85.9% of his income. That is genuinely impressive discipline. It is also not a blueprint for someone earning $53,000, which is the average individual income in the US.

On a $53,000 gross salary, take-home pay after federal and state taxes is roughly $40,000 to $43,000 depending on state, around $3,400 per month. The average American household spends about $6,500 per month according to BLS data, but that includes dual-income households. A single person on $53,000 has a different baseline.

Extreme frugal living at a normal income is not saving 85%. It is getting your savings rate from the national average of about 4% to somewhere between 20% and 35%. That is the realistic version of aggressive frugality and it is worth pursuing. It means saving $680 to $1,190 per month on that income, which compounds into real money over three to five years.

On a $53,000 salary, going from a 4% savings rate to a 25% savings rate means saving an additional $875 per month. Over five years with a 4% return in a high-yield savings account, that’s $57,900. That’s what extreme frugal living actually delivers at a normal income. Not $200k in one year. $57,900 over five years that you didn’t have before.

Extreme Frugal Living Strategies Worth the Sacrifice

These are the cuts that genuinely move the savings rate without destroying quality of life in ways that make the whole project unsustainable.

Housing: the biggest lever by far

Housing is the largest expense in most budgets and the most underdiscussed in frugality content because the advice is uncomfortable. The standard extreme frugal living moves on housing are: house hacking (buying a small multi-unit property and renting out the other units), getting a roommate, moving to a cheaper city or neighborhood, or negotiating rent aggressively at renewal.

The math dwarfs everything else. Cutting your housing cost by $400 a month, through a roommate or a cheaper apartment, saves $4,800 per year. That is more than switching to store-brand groceries for a decade. If housing is more than 35% of your take-home pay, it is the problem. Everything else is optimization noise until that number moves.

Realistic annual saving: $2,400 to $9,600 depending on market and willingness to make changes

Transport: own less car

The average American spends $12,182 per year on vehicle costs according to AAA’s 2025 Your Driving Costs study. That includes depreciation, insurance, fuel, maintenance, and financing. This is the second biggest lever after housing.

Extreme frugal living on transport means: going from two cars to one, driving an older paid-off car instead of financing a new one, switching to a cheaper insurance provider, or in dense cities eliminating a car entirely. Going from a $500 monthly car payment plus insurance on a new vehicle to a paid-off car with lower insurance saves $300 to $600 per month with no lifestyle impact beyond the ego hit of driving something older.

Realistic annual saving: $3,600 to $7,200

Food: system over sacrifice

83% of Americans now consider themselves frugal according to a 2026 BestMoney study, with 60% cutting back on groceries and 58% cutting dining out. But cutting food spending without a system just means suffering with no structure. The system that actually produces extreme frugal living results on food: meal plan every week, batch cook one item, eliminate delivery entirely, eat out once a week maximum as a planned expense rather than a default.

The full food system is covered in this breakdown of how to save money on food and this guide to saving money on groceries specifically. Combined, these changes save $200 to $400 per month for most households.

Realistic annual saving: $2,400 to $4,800

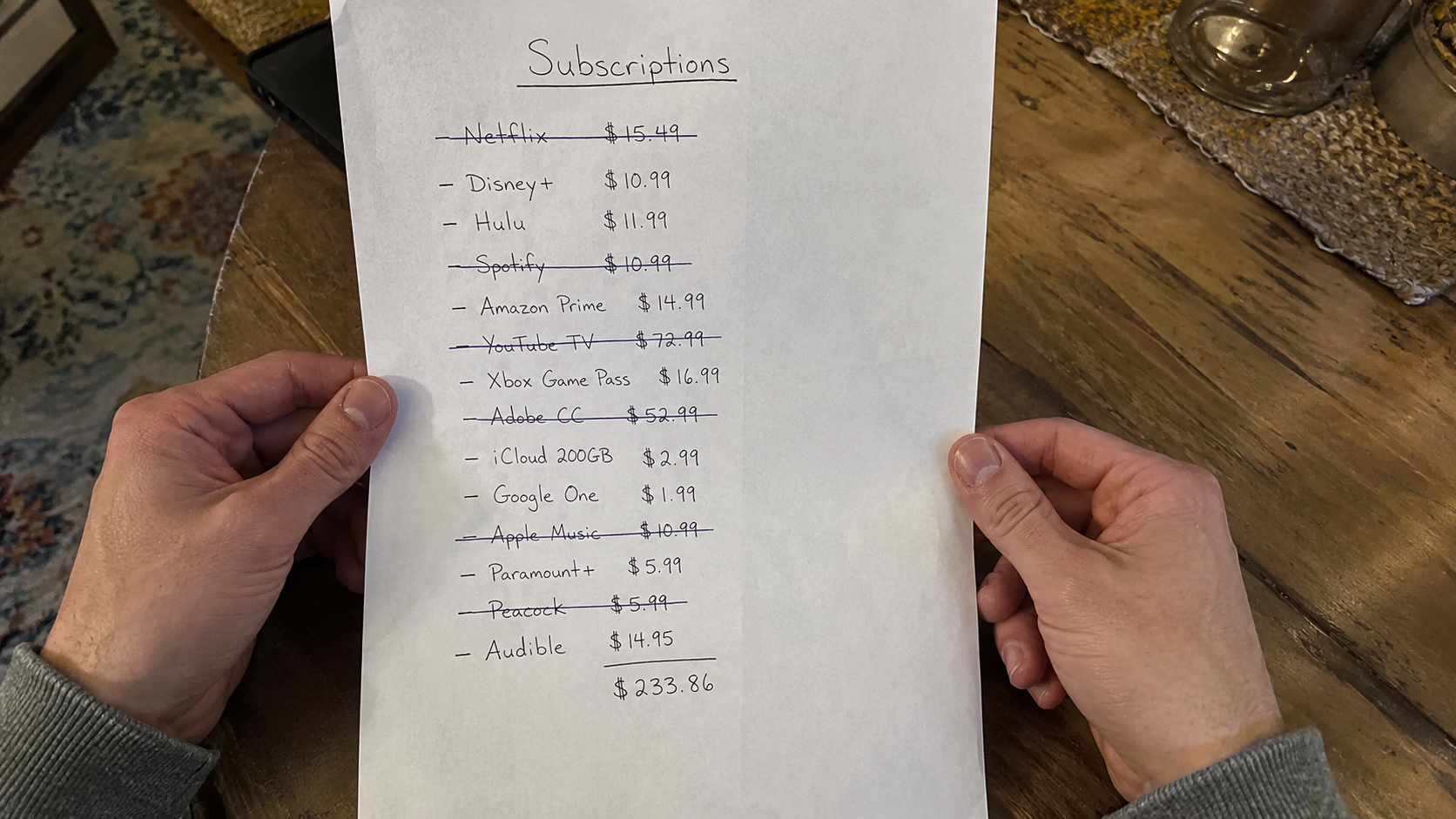

Subscriptions and recurring services: audit quarterly

The average American household spends $1,887 per year on subscriptions according to Fortunly’s 2026 subscription spending data, with $26.79 per month wasted on unused paid subscriptions. Extreme frugal living on subscriptions means cutting to the minimum viable set: one streaming service rotated every two months, no gym membership unless used more than 8 times per month, all software on free tiers where possible.

Realistic annual saving: $600 to $1,200

Where Extreme Frugal Living Stops Being Worth It

This is the part most frugality content skips. Every aggressive cut has three costs beyond the dollar amount: time cost, social cost, and sustainability cost. When any of these exceeds the dollar saving, the cut is not worth making.

Time cost: your hours have a value

Making your own cleaning products takes 30 minutes and saves $8 per month. If your time is worth $15 per hour, you just lost money. DIY car maintenance saves real money if you have the skills and tools. It costs real money in time if you don’t and spend six hours on a job a mechanic would do in one.

Extreme frugal living is not about doing everything yourself. It is about cutting spending where the time cost is low relative to the saving. Negotiating your insurance takes 20 minutes and saves $461 per year. That is $1,384 per hour of your time. Making your own laundry detergent takes 45 minutes per month and saves $7. That is $9.33 per hour. One of those is worth doing. The other is not.

Social cost: frugality that isolates you will fail

Extreme frugal living that requires you to skip every social event, never eat out with friends, or constantly explain and justify your choices to people around you creates a sustainability problem. Social isolation increases stress, and stress spending is a documented pattern where deprivation leads to compensatory purchases that cost more than the savings generated.

The fix is not hiding your frugality. It is building a social life around low-cost activities: cooking at home for friends instead of restaurants, free outdoor activities, potlucks instead of dinners out. The goal is not no social spending. It is social spending that fits the budget rather than social spending that happens by default because you haven’t built an alternative.

Sustainability cost: if it feels like punishment, it won’t last

The research on extreme dieting and extreme budgeting shows the same pattern. Severe restriction works in the short term and fails in the medium term because deprivation accumulates into a breaking point. The breaking point spending event, the vacation you put on a card after six months of extreme austerity, often costs more than the gradual spending would have.

Extreme frugal living that works long term always includes a fun money budget, however small. $50 to $100 per month of completely unjustified spending is not a failure of frugality. It is the pressure valve that makes the rest of the system sustainable.

George Kamel of Ramsey Solutions notes that excessive frugality can make you miserable and lead you to give up entirely. The advice: make intense frugality temporary when you need to accelerate toward a specific goal, not a permanent identity. Use it to build the emergency fund or eliminate a debt, then dial back to a sustainable savings rate.

What Extreme Frugal Living Actually Saves Across All Categories

| Category | Aggressive Cut | Annual Saving | Time Cost |

|---|---|---|---|

| Housing | Roommate or cheaper unit | $2,400 to $9,600 | One-time effort |

| Transport | Paid-off car, cheaper insurance | $3,600 to $7,200 | One-time decision |

| Food | Meal plan, batch cook, no delivery | $2,400 to $4,800 | Low once habitual |

| Subscriptions | Minimum viable set | $600 to $1,200 | One-time audit |

| Phone | Switch to MVNO | $480 to $1,440 | One 20-min call |

| Impulse buying | 48-hour rule, delete apps | $1,700 to $2,400 | Environmental setup |

| Total | $11,180 to $26,640/yr |

On a $40,000 take-home salary, $11,180 saved is a 28% savings rate. $26,640 is 67%. The realistic target for most people doing extreme frugal living seriously is somewhere in the $11,000 to $16,000 range, which represents a 27% to 40% savings rate. That is genuinely life-changing over a five to ten year horizon without requiring misery.

How to Start Extreme Frugal Living Without Burning Out in Month Two

Extreme frugal living without a target is just deprivation. Extreme frugal living aimed at a $20,000 emergency fund in 18 months is a project with an end date. The psychology is completely different. Temporary sacrifice for a defined outcome is sustainable. Open-ended austerity is not.

These two categories represent 50 to 60% of most household budgets. If you spend six months optimizing groceries and subscriptions while paying $400 over market rate for your apartment and financing a new car, you are working on the wrong problems. The big categories first. Everything else after.

Whatever your target savings rate is, set up an automatic transfer on payday before the money hits your spending account. This is the pay yourself first principle applied to an aggressive savings rate. The behavioral research is clear: money that never appears in your checking account doesn’t feel like a loss. Money you try to transfer manually at the end of the month after you’ve already spent it doesn’t exist.

Not as a reward for good behavior. As a structural component of the system. $75 per month of completely unjustified spending is the pressure valve that makes the other $875 in savings sustainable. Trying to run extreme frugal living with zero discretionary budget is like trying to diet with zero allowed indulgences. The research on both says the same thing: the all-or-nothing approach fails at a higher rate than the structured moderation approach.

Extreme Frugal Living Works When It Has a Target and a Timeline

Extreme frugal living on a normal income is not about saving 85% of a $234,000 salary. It is about going from a 4% savings rate to a 25% or 30% savings rate through a combination of one-time structural changes and sustained behavioral habits.

The structural changes are housing and transport. They are uncomfortable to address and produce the most money. The behavioral habits are food, subscriptions, impulse buying, and phone costs. They require consistency and produce real compounding savings over time.

The frugality that fails is the kind without a goal, without a fun money budget, and built entirely around small optimizations while ignoring the large fixed costs. The frugality that works looks like a project: specific target, aggressive savings rate, automated transfers, and a clear end date when you dial back to maintenance mode.

If you want a budgeting system to run alongside an aggressive savings rate, this guide to choosing the right budgeting method will match you with the one that fits how you actually live. And once you have savings accumulating, here’s where to keep them so they earn a real return while you build toward the goal.

")

{kind=link}