It’s a pattern that shows up constantly: no lavish spending, no big trips, just regular life. And yet by the 20th of every month the account looks like it’s been robbed. The money went somewhere. Nobody knows where.

The fix is also consistent: a real look at three months of bank statements. What turns up is never one big problem. It’s thirty small ones. Subscriptions nobody remembers signing up for. Groceries that got wasted. Habits that got monetized without anyone noticing.

If you’re trying to figure out how to cut monthly expenses without feeling like you’re punishing yourself, this is the honest version of that conversation.

According to the U.S. Bureau of Labor Statistics, the inflation rate hit 3.8% as of April 2026. Energy costs jumped 17.9% year over year. Food prices are up 2.3%. Your paycheck almost certainly did not keep pace with any of that.

The math got harder. That is not a mindset problem. That is reality. But there is real ground to reclaim if you know where to look.

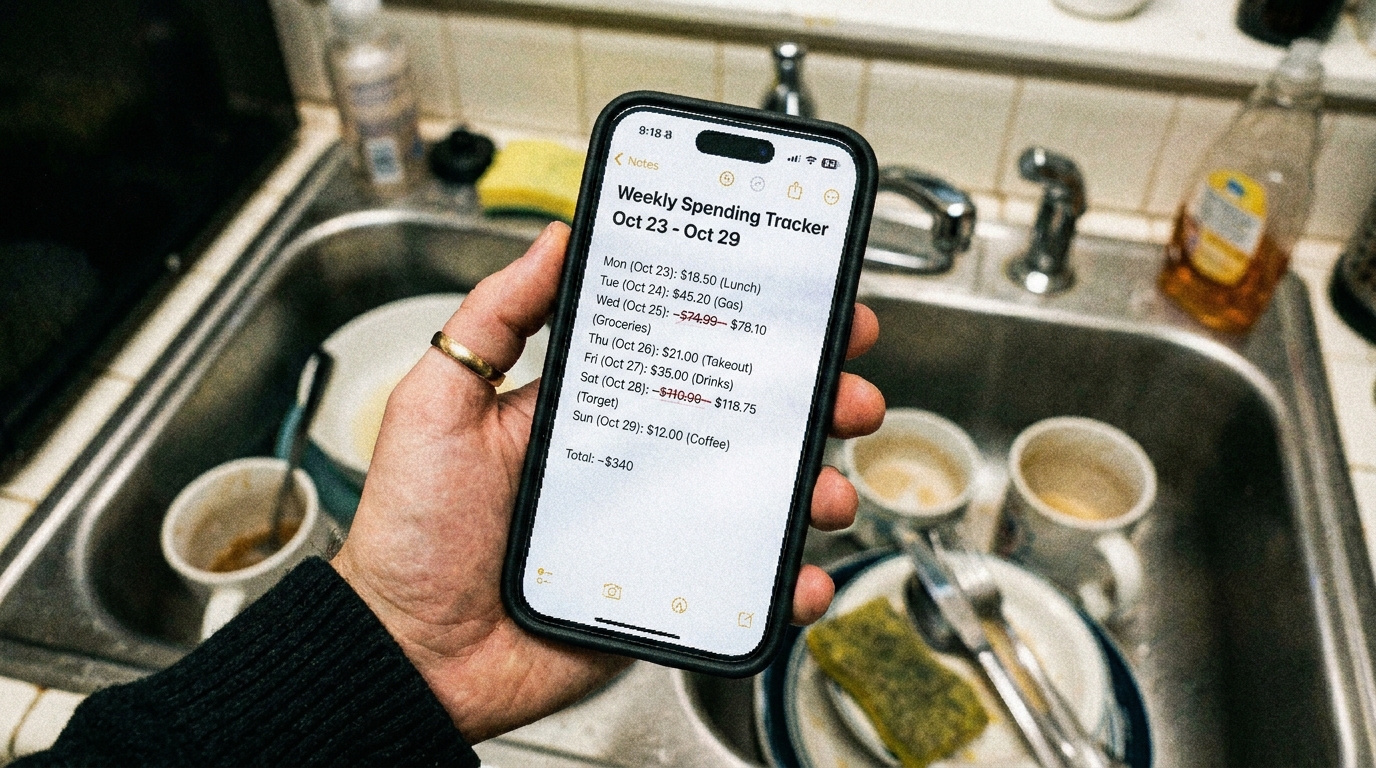

Start With the Audit You’ve Been Avoiding

Before you can cut monthly expenses, you need to know where the money is actually going. Not where you think it’s going, where it actually goes.

Pull three months of bank and credit card statements. Categorize every transaction: fixed costs (rent, insurance, loan minimums), variable spending (groceries, fuel, dining), and subscriptions. Don’t judge yet. Just look.

YNAB forces you to assign every dollar a job before you spend it, the most effective system for people who keep running out of money mid-month. Empower is better if you want a passive overview that also tracks investments. Both surface patterns your brain has been hiding from you.

Most people find at least two or three subscriptions they forgot about. Search your email for “receipt,” “subscription,” and “billing.” You will uncover charges that never made it into your mental budget.

No exceptions. If you genuinely miss it after a month, resubscribe, often at a promotional rate. These companies built monthly billing specifically because most people won’t cancel even when they’ve stopped using the service.

For streaming: rotate instead of stacking. Subscribe to one service for two months, cancel, move to the next. Most households running three to five streaming services simultaneously could cut two without noticing.

How to Cut Monthly Expenses on Groceries

Food is where most household budgets quietly bleed, and one of the fastest places to cut monthly expenses. It’s not one big purchase, it’s a hundred small decisions made while hungry and distracted.

The grocery store is engineered to make you spend more. The fix isn’t willpower, it’s a system.

Every impulse buy was planned by someone else

Five dinners planned. A list written from what you actually need. The alternative is buying ingredients for three meals, cooking one, and throwing out the rest. Most households waste a significant amount of food this way before they start planning.

Canned goods, pasta, rice, oils, frozen vegetables, cleaning products, paper products. Switch about 15 staples to store brand versions. The savings per shop are modest. Across a year they are significant. Most people can’t taste the difference on the majority of them.

Check your fridge and cupboards before every shop. The single most effective way to stop buying duplicates of things you already have.

How to Reduce Monthly Expenses on Bills

Most people pay the same rate for internet, phone, and insurance for years without questioning it. Providers regularly offer better rates to new customers. Your loyalty means nothing to them financially.

Call your internet provider and ask what their current promotional rates are. If they won’t match, mention you’re considering switching. Insurance is worth shopping annually, NerdWallet makes comparison fast.

Not having a buffer makes everything more expensive. A car repair that hits when your account is at zero becomes credit card debt at high interest. That same repair with $500 set aside is just an annoying Tuesday.

Even $25 a week transferred automatically on payday adds up to $1,300 in a year. The key word is automatic, before you can spend it.

High-yield savings accounts pay meaningfully more than traditional bank savings. Ally, Marcus by Goldman Sachs, and SoFi are solid options.

Switch From Monthly to Weekly Budgeting to Cut Monthly Expenses Faster

Monthly budgets are easy to blow in the first two weeks and spend the rest of the month rationalizing. A weekly variable-spend limit creates a tighter feedback loop that most people find easier to stick to.

Pick one number for all your variable spending: groceries, fuel, dining, miscellaneous. Reset it every Monday. If you blow it by Wednesday, you feel it by Friday. That friction is useful, it is information about your actual habits that a monthly budget hides from you.

Setting your weekly limit based on what you wish you spent instead of what you actually spend. Look at three months of real data first. The honest number will probably be higher than you expect.

Apps that make this easier

|

YNAB

Best for people who want a real system. Forces you to budget proactively rather than track reactively. |

Empower

Better if you also want to track investments and net worth alongside spending. |

Copilot

Clean iOS app with excellent visual breakdowns. Good for people who find YNAB too intensive. |

Common Mistakes to Skip

| 01 |

Cutting everything at once after a bad month

Canceling six subscriptions and switching to meal prepping every Sunday in a single panicked weekend sounds productive. In practice, almost nobody keeps all of it going after two weeks. One change at a time sticks. Six at once doesn’t. |

| 02 |

Ignoring the small recurring charges

Six things at $8 a month is $576 a year. Individual charges get dismissed as not worth worrying about. They absolutely are when you add them up. |

| 03 |

Not automating savings

Saving whatever is left at the end of the month means saving nothing, because there is never anything left. Treating savings like a bill you pay on payday is the only version that works. |

| 04 |

Budgeting based on optimism instead of history

Setting grocery budgets based on what you think you should spend, not what you actually spent. Real data changes behavior. Aspirational targets don’t. |

You don’t need to live smaller. You need to stop funding things you don’t value.

Learning how to lower monthly bills and reduce monthly expenses isn’t about restriction, it’s about redirecting. Every dollar you stop spending on a forgotten subscription or an unplanned grocery run is a dollar that can go somewhere that actually matters. The system above isn’t complicated. The hard part is just starting the audit. Once you see the numbers, the decisions usually make themselves.

Once you have expenses under control, the next step is making your savings work harder. The best high yield savings accounts in 2026 are paying over 4% APY. If you want a simple system for making savings happen automatically before you spend anything, the pay yourself first method is the easiest starting point. And if you want more structure for how you spend what is left, the cash envelope method works well alongside any expense-cutting effort. Not sure which system fits your situation? This guide to choosing the right budgeting method will point you in the right direction.

")

{kind=link}